Market sentiment pivoted on Thursday as shifting headlines around US-Iran peace talks drove a choppy and mixed session across asset classes, with equities extending their weekly advance and oil reversing a significant intraday gain on hopes that a Hormuz reopening could be approaching.

A dense global data slate, including a four-year high in US Manufacturing PMI, a near-complete collapse in the Philly Fed headline reading, and deeply disappointing services activity across the eurozone and UK, added layers of complexity to an already headline-sensitive session without resolving the central question traders have been asking for weeks: how close, exactly, is a deal.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand Balance of Trade for April 2026: 1.92B (0.8B forecast; 0.7B previous)

- Australia S&P Global Manufacturing PMI Flash for May 2026: 50.2 (50.6 forecast; 51.3 previous)

- Australia S&P Global Services PMI Flash for May 2026: 47.7 (49.9 forecast; 50.7 previous)

- Japan Balance of Trade for April 2026: 301.9B (-150.0B forecast; 667.0B previous)

- Japan Machinery Orders for March 2026: -9.4% m/m (-3.3% m/m forecast; 13.6% m/m previous); 5.9% y/y (18.0% y/y forecast; 24.7% y/y previous)

- Japan S&P Global Manufacturing PMI Flash for May 2026: 54.5 (54.0 forecast; 55.1 previous)

- Japan S&P Global Services PMI Flash for May 2026: 50.0 (50.7 forecast; 51.0 previous)

- Australia Consumer Inflation Expectations for May 2026: 5.6% (6.3% forecast; 5.9% previous)

-

Australia Employment Change for April 2026: -18.6k (10.0k forecast; 17.9k previous)

- Australia Unemployment Rate for April 2026: 4.5% (4.3% forecast; 4.3% previous)

- New Zealand Credit Card Spending for April 2026: 2.9% y/y (1.9% y/y forecast; 2.1% y/y previous)

- Swiss Industrial Production for Q1 2026: -7.1% y/y (0.5% y/y forecast; -0.7% y/y previous)

- Euro area Current Account for March 2026: 24.1B (32.0B forecast; 21.09B previous)

- Euro area S&P Global Manufacturing PMI Flash for May 2026: 51.4 (51.5 forecast; 52.2 previous)

- Euro area S&P Global Services PMI Flash for May 2026: 46.4 (48.0 forecast; 47.6 previous)

- U.K. S&P Global Manufacturing PMI Flash for May 2026: 53.7 (53.2 forecast; 53.7 previous)

- U.K. S&P Global Services PMI Flash for May 2026: 47.9 (51.7 forecast; 52.7 previous)

- U.K. CBI Industrial Trends Orders for May 2026: -41.0 (-40.0 forecast; -38.0 previous)

- U.S. Building Permits Prel for April 2026: 5.8% m/m (0.5% m/m forecast; -11.4% m/m previous)

- U.S. Initial Jobless Claims for May 16, 2026: 209.0k (210.0k forecast; 211.0k previous)

- U.S. Philadelphia Fed Manufacturing Index for May 2026: -0.4 (19.0 forecast; 26.7 previous)

- U.S. S&P Global Manufacturing PMI Flash for May 2026: 55.3 (53.0 forecast; 54.5 previous)

- U.S. S&P Global Services PMI Flash for May 2026: 50.9 (51.1 forecast; 51.0 previous)

- Euro area Consumer Confidence Flash for May 2026: -19.0 (-22.0 forecast; -20.6 previous)

- U.S. Kansas Fed Manufacturing Index for May 2026: 9.0 (9.0 forecast; 10.0 previous)

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

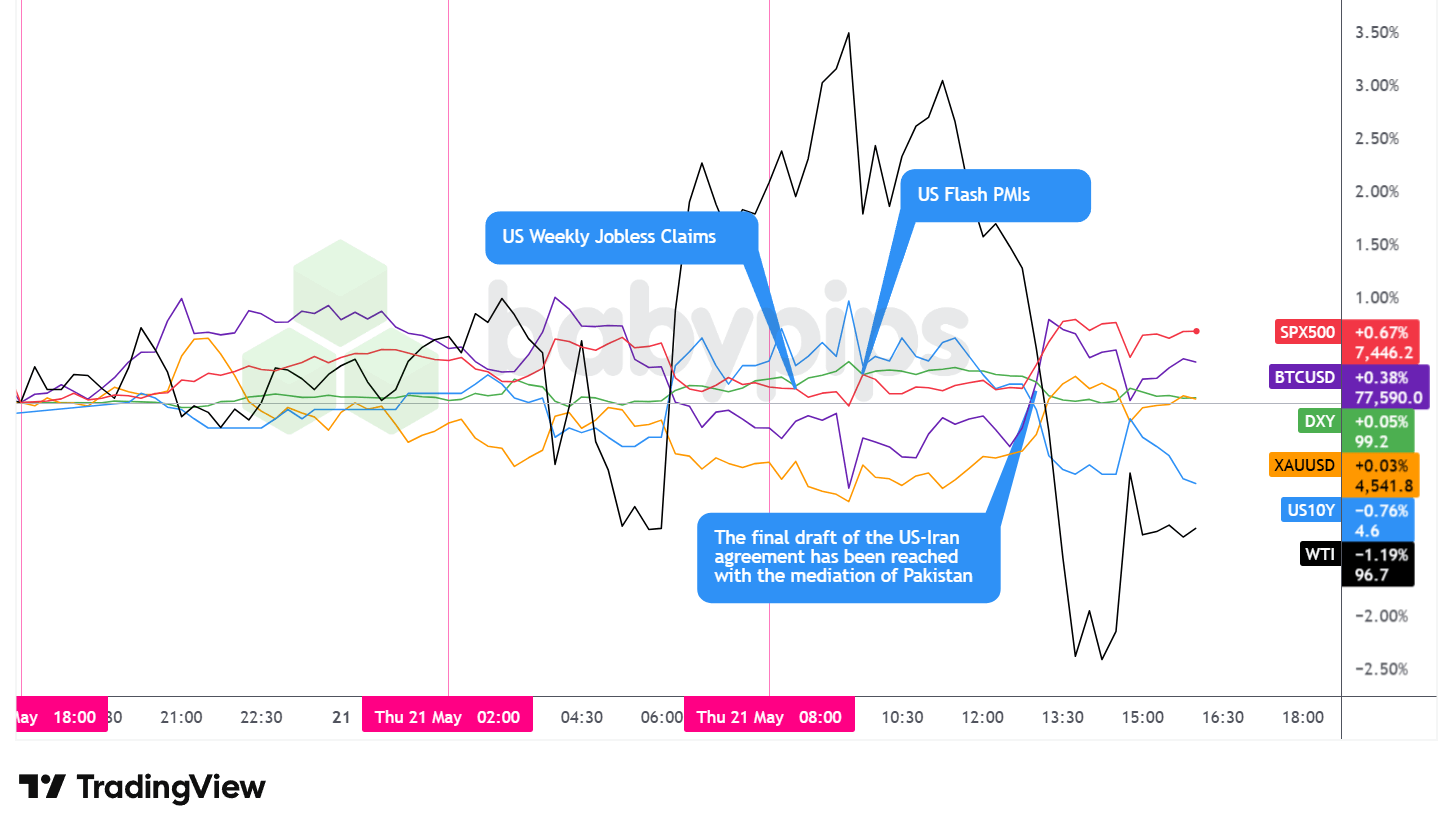

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session was shaped by a single overriding narrative: the prospect of a US-Iran peace agreement and what it might mean for the Strait of Hormuz. Markets swung around midday after reports circulated suggesting a final draft agreement had been reached via Pakistani mediation, triggering a sharp sell-off in oil and a spike in equities before risk appetite stabilized into the close. US economic data added conflicting signals throughout the day, with a historically strong Manufacturing PMI reading offset by a near-complete collapse in the Philly Fed headline print.

The S&P 500 advanced approximately 0.67% to close around 7,446, logging another gain for the week. The index navigated a choppy intraday path, dipping toward the 7,395 area during the London session before recovering through the US morning on solid jobs and PMI data, then spiking to a session high near 7,467 around the time of the Iran deal headlines. A modest pullback into the close still left equities in positive territory, with geopolitical optimism outweighing lingering uncertainty about whether a deal would actually materialize.

WTI crude oil was the session’s standout underperformer, declining approximately 1.19% to close near $96.70 per barrel. Oil had rallied sharply through the London session, reaching a high above $101.50, before reversing abruptly into and through the US afternoon. The sharp decline closely tracked the timing of the Iran deal headlines, which may have triggered speculation about a potential Hormuz reopening and the resumption of normal tanker flows. Oil’s net loss on the day, from what had been a significant intraday gain, underscored how sensitive energy markets remain to any perceived change in the conflict’s trajectory.

Gold ended essentially flat, up roughly 0.03% to approximately $4,542 per ounce. The precious metal had traded with notable intraday volatility, touching a session low near $4,489 during London hours before recovering through the US afternoon. The near-unchanged close possibly reflected competing forces: safe-haven demand tied to ongoing geopolitical uncertainty pulling against improving risk sentiment as peace deal optimism grew through the session.

Bitcoin edged modestly higher, gaining approximately 0.38% to around $77,590. The cryptocurrency traded in a wide intraday range between roughly $76,634 and $78,091, with price action tracking broader risk sentiment loosely rather than any crypto-specific catalyst. The muted net gain was consistent with a session where risk appetite improved but without the kind of broad-based surge that typically lifts speculative assets more aggressively.

The US 10-year Treasury yield fell approximately 0.76% on the day to around 4.60%, despite spending much of the earlier session trading higher. Yields climbed into the London open and reached a session high near 4.63% before reversing sharply in the US afternoon, a move that appeared to correlate with the Iran deal headlines and the corresponding drop in oil prices. A Hormuz reopening, if realized, would likely reduce the energy-driven inflation premium currently embedded in longer-dated yields, which may help explain the magnitude and timing of the reversal.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

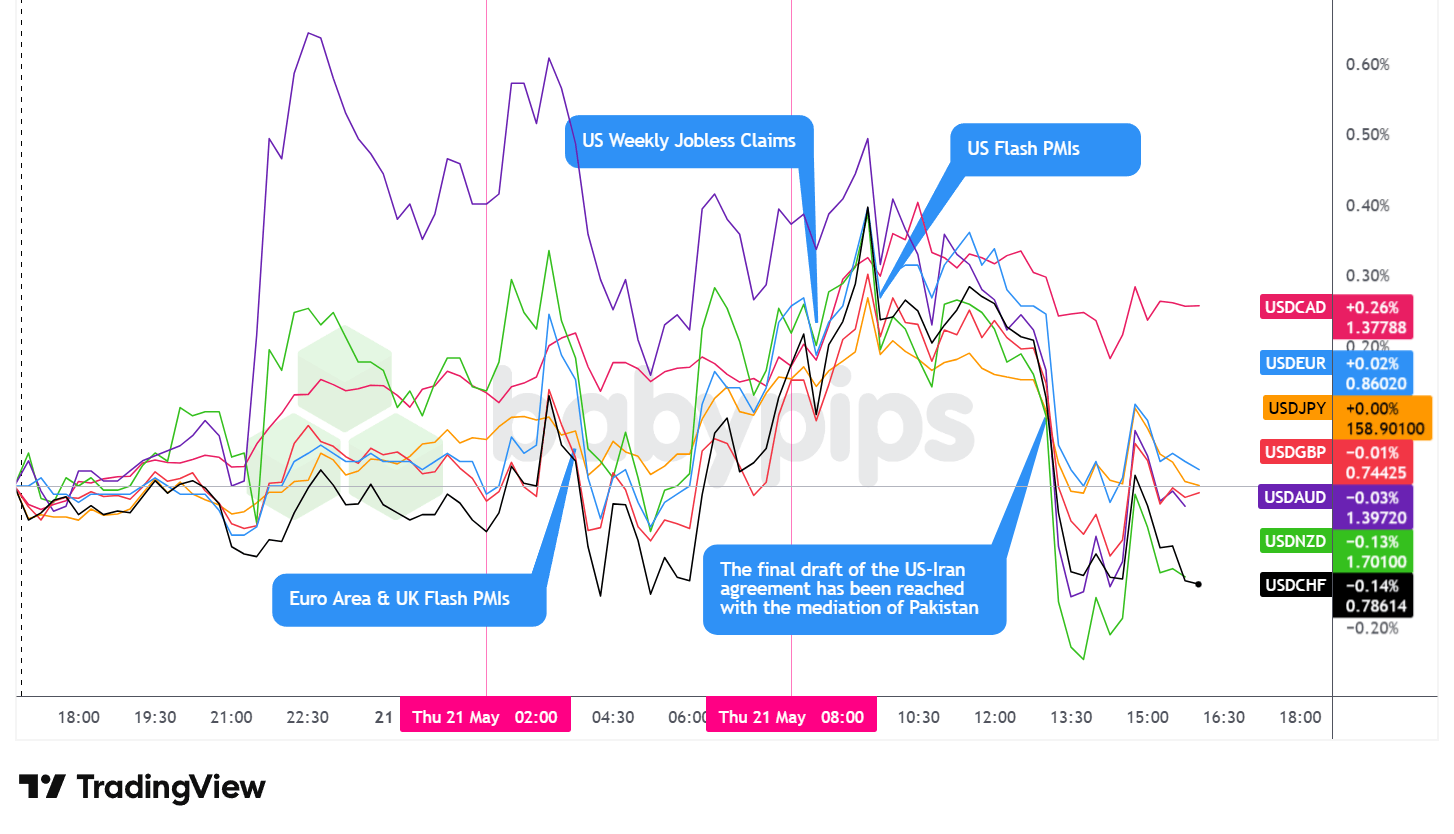

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded with a broadly firmer tone from the Asian session through the early US morning before a sharp midday pullback tied to Iran deal headlines, ultimately closing mixed but arguably net positive against the major currencies.

During the Asian session, the dollar traded net higher against the major currencies. The session delivered a heavy data flow from across the Asia-Pacific region, though the broader dollar tone appeared underpinned regardless of the individual releases. The most significant catalyst was Australia’s April employment report, which printed a loss of 18,600 jobs against expectations of a 17,500 gain, driving the unemployment rate to 4.5%, its highest reading since November 2021. The data triggered a sharp repricing of RBA rate expectations, with August hike probability collapsing from around 81% to 42%.

Japan’s trade data delivered a surprise surplus of 301.9 billion yen against a forecast deficit, as exports surged 14.8% year-on-year, though the headline was complicated by a 64% collapse in crude oil import volumes, reflecting supply disruption rather than organic demand improvement. BOJ board member Koeda’s hawkish remarks, signaling that underlying inflation is around 2% and that rates need to continue rising, provided some incremental support for the yen.

The London session brought flash PMI readings across the eurozone and UK that painted a picture of broadening contraction risk. The euro area services PMI fell to 46.4, its weakest reading in over two years, while the UK services PMI delivered a sharp miss, sliding to 47.9 from 52.7 against a 51.7 forecast. Manufacturing held up comparatively better on both sides of the Channel, but the composite readings pointed to deteriorating activity. ECB sources indicating that a June rate hike is nearly certain but July off the table added a nuanced backdrop to European FX. The dollar held its net higher posture from the Asian session through the London close.

During the US session, the dollar initially maintained its firmer tone following the release of US Weekly Jobless Claims and the Philly Fed data. Claims came in at 209,000, slightly below the 210,000 forecast and extending their recent improvement. The Philly Fed Manufacturing Index delivered a stark miss, falling to -0.4 against a 19.0 forecast and a 26.7 prior reading, with new orders also contracting sharply.

US Flash PMI data released shortly after told a different story, with the Manufacturing PMI coming in at 55.3, well above the 53.0 forecast, consistent with reporting that US manufacturing expanded at its fastest pace in four years as customers front-loaded orders ahead of mounting price pressures. The conflicting signals kept the dollar in a choppy but generally firm range through late morning.

Around 1:00 PM ET, headlines began circulating suggesting a final draft US-Iran agreement had been reached via Pakistani mediation, sparking a sharp and rapid decline in the dollar against most major currencies. The reversal appeared consistent with a repricing of geopolitical risk premium tied to hopes of a Hormuz reopening, with oil prices dropping sharply at the same time. The dollar found support relatively quickly, however, as subsequent commentary, including Secretary of State Rubio’s characterization of “some good signs” rather than a confirmed deal, introduced caution around the headline. The dollar stabilized and traded choppy through the remainder of the session, recovering a meaningful portion of the midday decline.

At Thursday’s close, the dollar was mixed against the major currencies but arguably net positive for the day, with commodity-linked and safe-haven currencies showing the most sensitivity to the midday geopolitical headlines.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (

4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution. Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Balance of Trade for April 2026 at 10:45 pm GMT

- Australia S&P Global Manufacturing & Services PMI Flash for May 2026 at 11:00 pm GMT

- Japan Balance of Trade for April 2026 at 11:50 pm GMT

- Japan Machinery Orders for March 2026 at 11:50 pm GMT

- Japan S&P Global Manufacturing & Services PMI Flash for May 2026 at 12:30 am GMT

- Australia Consumer Inflation Expectations for May 2026

- Australia Westpac Leading Index for April 2026

- Australia Employment Situation update for April 2026 at 1:30 am GMT

- Bank of Japan Koeda Speech at 1:30 am GMT

- New Zealand Credit Card Spending for April 2026 at 3:00 am GMT

- Swiss Industrial Production for March 31, 2026 at 6:30 am GMT

- Euro area S&P Global Manufacturing & Services PMI Flash for May 2026 at 8:00 am GMT

- U.K. S&P Global Manufacturing & Services PMI Flash for May 2026 at 8:30 am GMT

- Euro area Labour Cost Index Flash for March 31, 2026 at 9:00 am GMT

- U.K. CBI Industrial Trends Orders for May 2026 at 10:00 am GMT

- U.S. Building Permits & Housing Starts for April 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for May 16, 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for May 2026 at 12:30 pm GMT

- Bank of England Taylor Speech at 1:00 pm GMT

- U.S. S&P Global Manufacturing & Services PMI Flash for May 2026 at 1:45 pm GMT

- Euro area Consumer Confidence Flash for May 2026 at 2:00 pm GMT

- U.S. Kansas Fed Manufacturing Index for May 2026 at 3:00 pm GMT

Japan’s April CPI print overnight will be watched carefully given BOJ board member Koeda’s hawkish commentary Thursday, with a reading above consensus likely reinforcing the case for continued BOJ rate hikes and adding pressure to USD/JPY.

UK Retail Sales Friday morning will attract attention given Thursday’s UK services PMI collapse to 47.9, with the data potentially shedding further light on the degree of consumer softness in the UK economy.

The University of Michigan Consumer Sentiment Index will be monitored for signs of US consumer anxiety around energy prices, particularly relevant given Walmart’s warning Thursday that rising fuel costs are squeezing margins and could translate to higher prices for shoppers.

Fed Governor Waller’s 3:00 PM GMT appearance will be closely watched for any updated guidance on the rate path, given Thursday’s contradictory data signals: a sharp Philly Fed miss alongside a four-year high in the Manufacturing PMI. Any material development in US-Iran talks over the weekend or Friday morning remains the dominant wildcard across oil, yields, and FX.

Stay frosty out there, forex friends!

Thursday’s sharp midday reversal shows what most traders miss: how geopolitical headlines shift the market’s appetite for risk, and which currencies benefit when traders flip from cautious to optimistic. Premium members can read our lesson:

Risk-On / Risk-Off: How Global Mood Moves Currencies Reading this helps you understand which currencies win when traders feel bold, which ones win when they get scared, and how to check the risk weather before placing any trade.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what moved today, but the structural risk-on/risk-off dynamics that move currencies every single day, so you can read the market’s mood before the next headline hits.

{kind=link}