Thursday’s markets were whipsawed by conflicting US-Iran war headlines, swinging from risk-off on renewed Strait of Hormuz clashes to risk-on on ceasefire extension reports.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. API Crude Oil Stock Change for May 22, 2026: -2.8M (-9.1M previous)

- U.K. Car Production for April 2026: -0.7% y/y (13.5% y/y forecast; -0.8% y/y previous)

- Australia Household Spending for April 2026: 4.9% y/y (5.5% y/y forecast; 6.3% y/y previous)

- Swiss Non Farm Payrolls for Q1 2026: 5.54M (5.4M forecast; 5.54M previous)

- Euro area Economic Sentiment for May 2026: 93.5 (91.0 forecast; 93.0 previous)

- Canada Average Weekly Earnings for March 2026: 3.5% y/y (2.1% y/y forecast; 3.4% y/y previous)

- U.S. Building Permits Final for April 2026: 4.4% m/m (5.8% m/m forecast; 11.0% m/m previous)

- U.S. Initial Jobless Claims for May 23, 2026: 215.0k (215.0k forecast; 209.0k previous)

- U.S. GDP Growth Rate 2nd Est for Q1 2026: 1.6% q/q (2.0% q/q forecast; 0.5% q/q previous)

-

U.S. Core PCE Price Index for April 2026: 3.3% y/y (3.3% y/y forecast; 3.2% y/y previous); 0.2% m/m (0.3% m/m forecast; 0.3% m/m previous)

- U.S. Personal Income for April 2026: 0.0% m/m (0.5% m/m forecast; 0.6% m/m previous)

- U.S. Personal Spending for April 2026: 0.5% m/m (0.6% m/m forecast; 0.9% m/m previous)

- U.S. Durable Goods Orders for April 2026: 7.9% m/m (3.4% m/m forecast; 0.8% m/m previous)

- U.S. New Home Sales for April 2026: -6.2% m/m (-3.2% m/m forecast; 7.4% m/m previous)

- U.S. EIA Crude Oil Stocks Change for May 22, 2026: -3.33M (-7.86M previous)

- US and Iran tentatively agree to a 60-day ceasefire extension and further nuclear talks, pending President Trump’s approval — Axios reported the development mid-session, sparking a broad risk-on shift across equities, bonds, and currencies. Treasury Secretary Scott Bessent declined to confirm a deal, saying only that “the teams have been going back and forth,” and reaffirmed that Trump’s three red lines — reopening the Strait of Hormuz, Iran surrendering highly enriched uranium, and ending its nuclear program — remain non-negotiable.

- New York Fed President John Williams said the economy and labor market remain solid, that monetary policy is currently well-positioned, and that future decisions will remain data dependent.

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

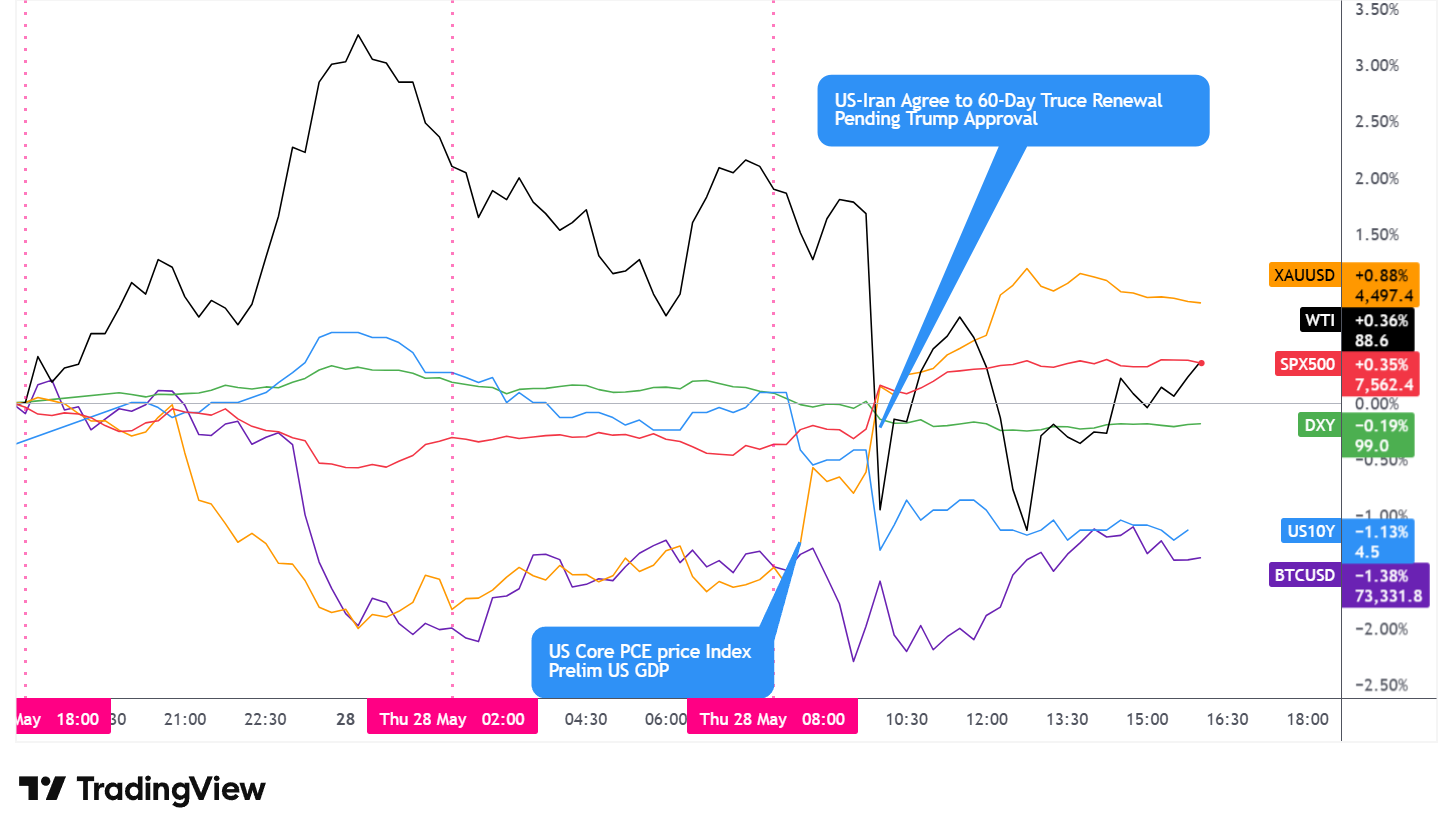

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session was defined by a sharp mid-session pivot as headlines confirming a tentative US-Iran 60-day ceasefire extension reversed an earlier risk-off tone driven by overnight clashes in and around the Strait of Hormuz.

The S&P 500 closed up roughly 0.35%, extending its winning streak to six consecutive sessions and notching fresh record highs. The index spent the overnight and early London hours under mild selling pressure, then swung sharply higher after the ceasefire extension reports crossed, rising through prior resistance levels and holding gains through the close. The rally came despite the US Q1 GDP second estimate being revised down to 1.6% annualized from an earlier print and softening consumer spending data, with traders appearing to give more weight to the peace-deal optimism than to the weaker growth figures.

WTI crude oil had the session’s most volatile arc. Prices surged to around $91 per barrel during the Asia session as Iran’s missile and drone attacks on Kuwait and a US air base raised acute fears of further Strait of Hormuz disruption. Prices then reversed sharply lower following the ceasefire extension reports, ultimately settling near $88.50, a modest gain on the day. The swing illustrated the market’s ongoing sensitivity to any shift in the perceived probability of Hormuz reopening.

Gold reversed its recent multi-session slide, closing up roughly 0.88% near $4,497 after recovering from Asia-session lows. The precious metal had fallen sharply overnight as the dollar strengthened on safe-haven demand during the Kuwait attack, but it recovered alongside the broader risk-on shift following the ceasefire headlines.

The 10-year Treasury yield fell approximately 0.62% on the day, closing near 4.45%. Yields pushed higher during the Asia session as geopolitical risk intensified, then reversed lower alongside the ceasefire optimism and a slightly softer-than-expected monthly core PCE reading of 0.2% versus 0.3% forecast. A well-received 7-year note auction also contributed to the move lower in yields.

Bitcoin declined roughly 1.4% to trade near $73,200. The cryptocurrency sold off during the Asia session alongside other risk assets, briefly bounced on the ceasefire headlines, then gave back those gains through the US afternoon, closing near session lows and underperforming the broader risk-on rally.

Promoted: The Prop Firm Built for Serious Traders.

Don’t let your trading strategy be held back by capital limitations. Alpha Capital Group offers access to simulated funded accounts from $5K to $200K, with entry prices starting as low as $40. They are distinguished by their features, including zero commissions, unlimited trading days during evaluation, and an 80% profit split. Start with a professional-sized account and scale your buying power up to $2M. Join 250K+ traders in 180+ countries today.

Learn more about Alpha Capital Group and current discount codes here!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

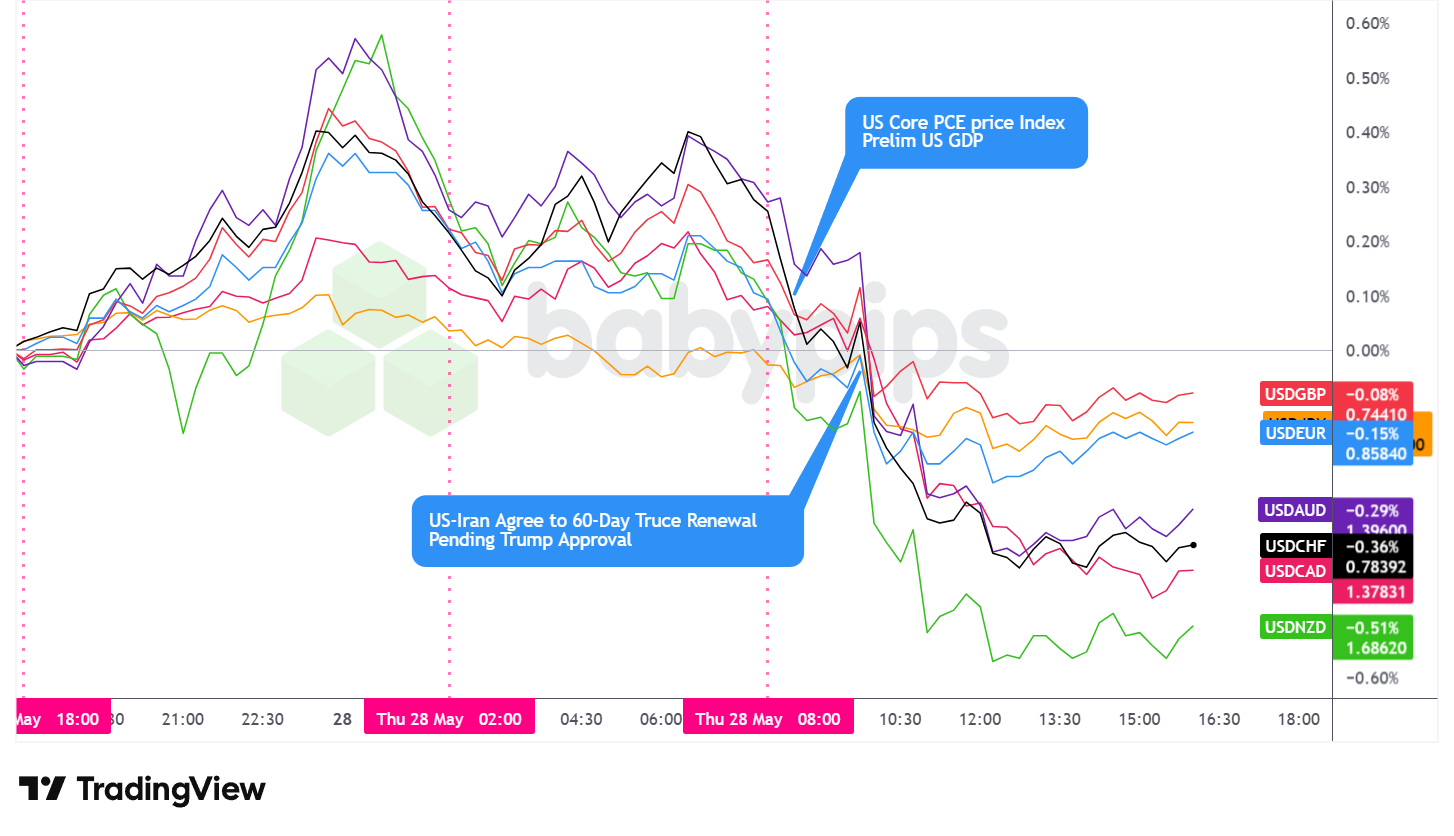

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar finished Thursday as the worst performer among the major currencies, closing broadly lower after spending the first half of the session in positive territory.

During the Asian session, the dollar traded net higher against the majors. The IRGC’s confirmed missile and drone attacks on Kuwait and a US air base drove acute risk aversion, and the greenback drew safe-haven demand as geopolitical tensions escalated. The move was broad-based, with the dollar pushing higher across commodity-linked and safe-haven currencies alike.

From roughly an hour ahead of the London open, the dollar began to turn lower, stabilizing through the early London session as the initial shock from the overnight headlines faded. European trading was relatively measured, though the tone remained cautious. The ECB’s April meeting accounts confirming intensified upside inflation risks and ECB policymaker Stournaras flagging a June hike as the most likely outcome possibly lent the euro some support, contributing to modest dollar softness through the morning.

The dollar turned decisively lower just ahead of the US session open as the core PCE report printed cooler than expected on a monthly basis at 0.2% versus 0.3% forecast. The move accelerated sharply when reports of a tentative 60-day US-Iran ceasefire extension crossed the wires, triggering a broad risk-on shift that undercut the greenback’s earlier safe-haven premium. Commodity-linked currencies led the advance, likely buoyed by the prospect of Hormuz reopening and an improvement in the global energy supply outlook. European currencies also firmed. The dollar stabilized through the US afternoon but was unable to reclaim meaningful ground.

At the Thursday close, the dollar had shed its Asia-session gains entirely, finishing net lower against all tracked majors, with commodity-linked currencies posting the largest gains.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (

4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution. Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand ANZ Roy Morgan Consumer Confidence for May 2026 at 10:00 pm GMT

- Japan Core CPI for May 2026 at 11:30 pm GMT

- Japan Unemployment Rate for April 2026 at 11:30 pm GMT

- Japan Tokyo CPI for May 2026 at 11:30 pm GMT

- Japan Industrial Production Prel for April 2026 at 11:50 pm GMT

- Japan Retail Sales for April 2026 at 11:50 pm GMT

- New Zealand ANZ Business Confidence for May 2026 at 1:00 am GMT

- Australia Housing & Private Sector Credit for April 2026 at 1:30 am GMT

- Japan Housing Starts for April 2026 at 5:00 am GMT

- Japan Consumer Confidence for May 2026 at 5:00 am GMT

- Germany Import Prices for April 2026 at 6:00 am GMT

- U.K. Nationwide Housing Prices for May 2026 at 6:00 am GMT

- Swiss KOF Leading Indicators for May 2026 at 7:00 am GMT

- Germany Unemployment Change for May 2026 at 7:55 am GMT

- Bank of England Gov Bailey Speech at 8:20 am GMT

- Germany Inflation Rate Prel for May 2026 at 12:00 pm GMT

- Canada GDP Growth Rate for March & April 2026 at 12:30 pm GMT

- U.S. Wholesale & Retail Inventories Adv for April 2026 at 12:30 pm GMT

- U.S. Goods Trade Balance Adv for April 2026 at 12:30 pm GMT

- U.S. Fed Bowman Speech at 1:10 pm GMT

- U.S. Fed Paulson Speech at 1:15 pm GMT

- U.S. Chicago PMI for May 2026 at 1:45 pm GMT

- Canada Budget Balance for March 2026 at 3:00 pm GMT

Friday’s calendar is front-loaded with Japan inflation data, where Tokyo CPI and national Core CPI will offer the most current read on whether war-driven energy costs are pushing Japanese prices higher and adding pressure on the Bank of Japan.

German preliminary May inflation could reinforce the ECB’s June hike case if it comes in firm. BoE Governor Bailey’s speech will be closely watched given that sterling has been trading with elevated sensitivity to any shift in the UK rate outlook.

Later in the US session, Fed speakers Bowman and Paulson may offer additional color on how policymakers are weighing the softer monthly PCE print against still-elevated annual readings. Any fresh US-Iran headlines over the weekend remain the dominant wildcard.

Stay frosty out there, forex friends!

Thursday’s session showed exactly what happens when geopolitical headlines hit the market, sending currencies and commodities through sharp reversals in minutes. But most traders don’t understand the mechanism that drives those moves. Premium members can read our lesson:

Geopolitical Risk, Trade Policy, and Safe Haven Flows Reading this helps you understand how geopolitical events move currencies, which safe havens benefit when the world breaks things, and how to position for the risk-on/risk-off swings that happen when headlines shift.

And if you’re not a Premium subscriber yet, now’s a good time to join.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the chart shows, but the macroeconomic and geopolitical forces behind every major move.

{kind=link}