Silver just spent the first half of 2026 swinging from record highs to a sharp crash. So what happens next?

Silver is part investment asset, like gold, and part industrial material, used in electronics and solar panels. That means it reacts to interest rates and the dollar just as much as it does to factory demand.

That combination of forces makes the second-half setup interesting, starting with the supply and demand picture.

Where silver stands right now

Silver dipped to seven-month lows near $55 an ounce before climbing back above $60. The bounce came as easing inflation expectations reduced pressure on the Federal Reserve to raise rates.

{kind=link}

That’s well off the metal’s all-time high. Silver broke out to new all-time highs above $121 per ounce in January 2026 amid a supply deficit, macro tailwinds, and a wave of speculative buying that later unwound sharply.

The round trip from over $120 back to around $60 likely cleared out a lot of speculative bets. It’s also a reminder of how fast this metal can move in either direction.

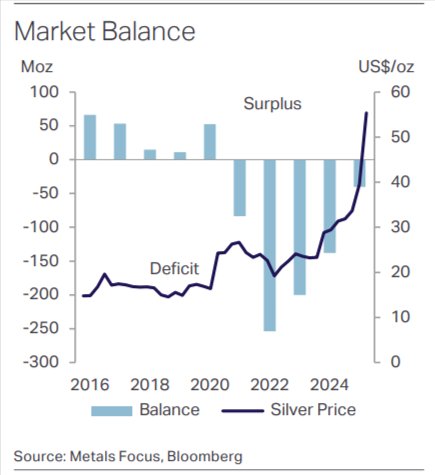

A supply deficit six years running

Silver has been running a supply deficit, meaning demand outpaces what mines and recycling produce, for years now.

Because over 70% of silver is mined as a secondary byproduct of copper, zinc, and lead, mining operations can’t easily ramp up production just because silver prices spike.

The Silver Institute’s latest World Silver Survey projects a 46.3 million ounce shortfall in 2026, widening from a 40.3 million ounce deficit in 2025.

That marks a sixth straight year of deficits.

That’s the core structural bull case: the silver market still doesn’t have enough metal.

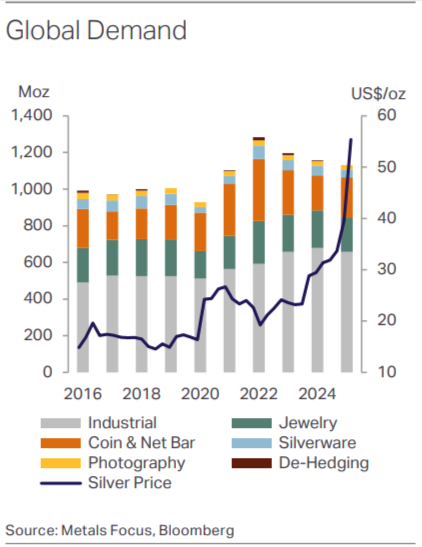

Demand pulling in two directions

On the demand side, investors and manufacturers are moving in opposite directions.

- Investment buying (bars and coins) is forecast to rise 18% in 2026, driven by a recovery in US retail buying.

- Industrial demand is heading the other way. It makes up 58% of total demand and is expected to ease another 3% in 2026, largely because solar panel manufacturers are thrifting and substituting away from silver faster than gains from AI infrastructure, autos, and power grid spending can offset.

What about AI demand?

It’s easy to assume AI’s boom would push silver demand up, not down.

AI demand for silver is real. The expansion of data centers, high-performance chips, and server infrastructure, along with the automotive sector, are expected to support silver consumption across a range of industrial end-uses, partially offsetting the decline in solar panel demand.

But “partially” is the key word. Solar’s silver intensity is falling faster than AI’s silver use is climbing, which is exactly why the industrial total is still negative overall.

AI is a genuine bright spot and one to watch, since a sharp acceleration in data center buildout is one of the more plausible ways this picture could improve faster than expected. It isn’t currently strong enough to flip industrial demand positive, though.

The net effect is a long-term backdrop that leans positive, but softening industrial use puts a ceiling on how far silver can climb without help from the macro side, like rates or the dollar.

It’s also why silver can behave differently from gold during a downturn.

Gold’s industrial use is a small slice of total demand, most of which comes from jewelry, investment, and central bank buying, so it’s barely affected by a manufacturing slowdown.

Silver’s industrial applications make up a much larger share of its total demand, so worries about a manufacturing slowdown can pull silver’s price down even during periods when gold is rising on safe-haven buying.

Three scenarios for the second half

Here’s how silver could play out in the second half of the year, depending on how macro headlines like Fed decisions or dollar moves shake out.

These are possible scenarios of what could happen under different conditions, not predictions of what will happen.

Bullish

Rates fall and the dollar weakens, which makes silver more attractive to hold since there’s less opportunity cost to owning an asset that pays no interest, and it becomes cheaper for buyers outside the US.

That extra buying comes on top of a market that already doesn’t have enough metal, described above, which can amplify price moves since there’s less available to absorb the demand.

In this scenario, silver could push back toward the upper part of its 2026 range, with quick rallies and shallow pullbacks as buyers step in on dips.

Base case

The Fed holds rates steady rather than cutting or hiking, and the dollar holds relatively firm.

Industrial demand stays soft but stable rather than collapsing, and investment demand remains solid but not explosive.

Under these conditions, silver likely trades in a wide sideways range around current levels, with sharp swings up and down but no clear long-term trend.

Bearish

The dollar keeps strengthening and the Fed becomes more hawkish, keeping real rates elevated.

Industrial demand weakens more than expected, and investment interest cools.

In this case, silver could retest or break below its recent lows, towards $50, with rallies fading quickly as traders focus on weaker industrial demand.

Scenario summary

Here’s the same breakdown side by side for quick reference.

| Scenario | What would cause it | What price action might look like |

|---|---|---|

| Bullish | Rates fall, the dollar weakens, and investment demand keeps growing, adding to a market that already doesn’t have enough metal | Price pushes toward the top of its 2026 range, with quick rallies and shallow dips |

| Base case | The Fed holds rates steady, the dollar holds firm, industrial demand stays soft but doesn’t collapse | Wide sideways range, choppy but without a clear trend |

| Bearish | Dollar keeps strengthening, the Fed turns more hawkish or hikes, real rates stay elevated, industrial demand weakens further, investment interest cools | Price retests or breaks below recent lows, rallies fade quickly |

What to watch

These are the signals that will tell you which scenario is playing out.

- Fed language on future rate moves.

- Dollar strength or weakness in coming months.

- Solar manufacturer earnings calls (e.g., First Solar (FSLR), JinkoSolar (JKS), Canadian Solar (CSIQ)) for signs of continued cuts to the amount of silver used per panel.

- Data center and AI infrastructure spending, since it’s the main offset to weaker solar demand

If these lean bullish, silver has room to grind higher.

If those forces turn bearish, weaker industrial demand and a stronger dollar could push silver back toward its recent lows first, with a deeper slide toward $50 becoming possible if selling pressure builds.