Markets swung wildly Thursday as hotter US PPI data crushed the “done deal” narrative for a September rate cut, sending Treasury yields and the dollar higher.

Stocks held firm, oil climbed, gold slipped, and traders braced for a packed Friday of data and the US–Russia meeting.

Here are headlines you may have missed in the last trading sessions!

Headlines:

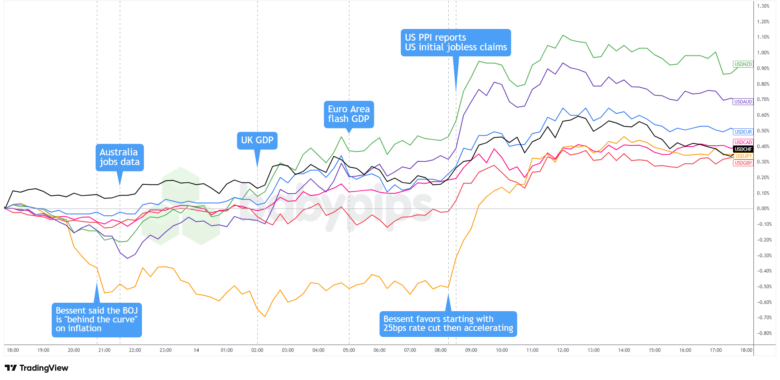

- US Treasury Secretary Bessent said BOJ is ‘behind the curve’ on inflation, thinks the central bank would be hiking rates

- AUD Rallied After Jobs Report Pushed RBA Rate Cut Odds Toward November

-

U.K. GDP growth rate prel for Q2 2025: 0.3% q/q (0.1% q/q forecast; 0.7% q/q previous); 1.2% y/y (0.7% y/y forecast; 1.3% y/y previous)

- U.K. GDP for June: 0.4% m/m (0.1% m/m forecast; -0.1% m/m previous); 1.4% y/y (1.0% y/y forecast; 0.7% y/y previous)

- U.K. industrial production for June: 0.7% m/m (0.3% m/m forecast; -0.9% m/m previous); 0.2% y/y (-0.2% y/y forecast; -0.3% y/y previous)

- U.K. goods trade balance for June: -22.16B (-21.5B forecast; -21.69B previous)

- Swiss producer & import prices for July: -0.2% m/m (0.1% m/m forecast; -0.1% m/m previous); -0.9% y/y (-0.6% y/y forecast; -0.7% y/y previous)

- Euro Area GDP growth rate 2nd est for Q2 2025: 0.1% q/q (0.1% q/q forecast; 0.6% q/q previous); 1.4% y/y (1.4% y/y forecast; 1.5% y/y previous)

- Euro Area industrial production for June: -1.3% (-0.6% forecast; 1.7% previous)

- US Treasury Secretary Bessent denied pressuring the Fed, said he favors 25bp rate cut before accelerating

- Bessent said US won’t buy more crypto for bitcoin reserve, will use seized assets instead

- U.S. initial jobless claims for August 9: 224.0k (228.0k forecast; 226.0k previous)

-

U.S. PPI for July: 0.9% m/m (0.2% m/m forecast; 0.0% m/m previous); 3.3% y/y (2.5% y/y forecast; 2.3% y/y previous)

- U.S. core PPI for July: 0.9% (0.1% forecast; 0.0% previous); 3.7% y/y (2.7% y/y forecast; 2.6% y/y previous)

- US President Trump said he’s seeking an ‘immediate peace deal’ with Putin rather than ceasefire

- U.K. NIESR monthly GDP for July: 0.2% (0.1% forecast; 0.2% previous)

- U.S. Fed balance sheet for August 13: 6.64 (6.64 previous)

- San Francisco Fed President Daly said a 50bps rate cut in September doesn’t seem warranted

- FOMC member Musalem thinks a 50bps rate cut would be unwarranted, said it’s too early to make a call on September rate decision

- Richmond Fed President Barkin sees improved consumer spending in July

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major assets were all over the charts Thursday after hotter US producer price inflation threw a wrench into September rate cut bets and pushed Treasury yields higher. July’s PPI jumped 0.9% from the previous month, the biggest spike in three years, hinting that companies are passing tariff costs down the line.

Stocks on Wall Street barely budged despite the inflation jolt, with the S&P 500 squeezing out a small gain to set another record close after dipping to 6,440 earlier in the day. Over in Europe, the DAX and CAC 40 both posted solid gains thanks to upbeat UK GDP data and optimism ahead of Friday’s Trump–Putin meeting in Alaska.

Treasury yields popped after the PPI report, with the 10-year moving up to 4.29% as traders dialed back September cut odds from “done deal” to about 90%. Gold slid to $3,335 on a stronger dollar and rising real yields, while bitcoin sank to $118,000 after Treasury Secretary Bessent made it clear the US isn’t buying crypto, only weighing what to do with seized assets. Oil went the other way, with WTI climbing to $63.95 on geopolitical jitters before the US–Russia talks.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Majors Chart by TradingView

The dollar started Thursday on a defensive footing as markets fully priced in a September rate cut following Tuesday’s benign CPI data and Treasury Secretary Bessent’s earlier dovish comments. USD/JPY bore the brunt of early selling pressure, sliding toward 146.40 after Bessent criticized the Bank of Japan for being “behind the curve” on inflation and urged rate hikes, compounding the pair’s weakness from broad dollar softness.

European hours saw modest dollar recovery, possibly as traders squared positions ahead of Thursday’s US data releases. The real catalyst came when July PPI surged 0.9%, the sharpest increase in three years. The dollar immediately surged across the board, with the DXY jumping from around 4.27 to test 4.29 resistance.

Bessent’s subsequent clarification that he wasn’t pressuring the Fed and favored starting with a measured 25 basis point cut before potentially accelerating further helped cement dollar gains. By London’s close, the Greenback had stabilized near session highs, posting broad gains of 0.4-0.5% against major currencies, with the antipodeans suffering the steepest losses.

Upcoming Potential Catalysts on the Economic Calendar

- Japan industrial production final for June at 4:30 am GMT

- Swiss GDP growth rate flash for June 30 at 7:00 am GMT

- Canada wholesale sales final for June at 12:30 pm GMT

- Canada new motor vehicle sales for June at 12:30 pm GMT

- Canada manufacturing sales final for June at 12:30 pm GMT

- U.S. retail sales for July at 12:30 pm GMT

- U.S. import and export prices for July at 12:30 pm GMT

- U.S. NY Empire State manufacturing index for August at 12:30 pm GMT

- U.S. industrial production for July at 1:15 pm GMT

- U.S. manufacturing production for July at 1:15 pm GMT

- U.S. University of Michigan consumer sentiment index for August at 2:00 pm GMT

- U.S. Michigan inflation expectations prel for August at 2:00 pm GMT

- U.S. business inventories for June at 2:00 pm GMT

- U.S. Baker Hughes oil rig count for August 15, 2025 at 5:00 pm GMT

- U.S.-Russia meeting on Ukraine peace deal scheduled today

Traders head into Friday with plenty on their plates, and the day kicks off with Swiss GDP that could set the early tone in London.

But the spotlight will quickly shift to a wave of US releases, from retail sales and import prices to factory output and Michigan sentiment, all dropping ahead of the highly anticipated US–Russia meeting.

As always, look out for global trade developments and geopolitical headlines that could influence overall market sentiment. Stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!

{kind=link}